TL;DR:

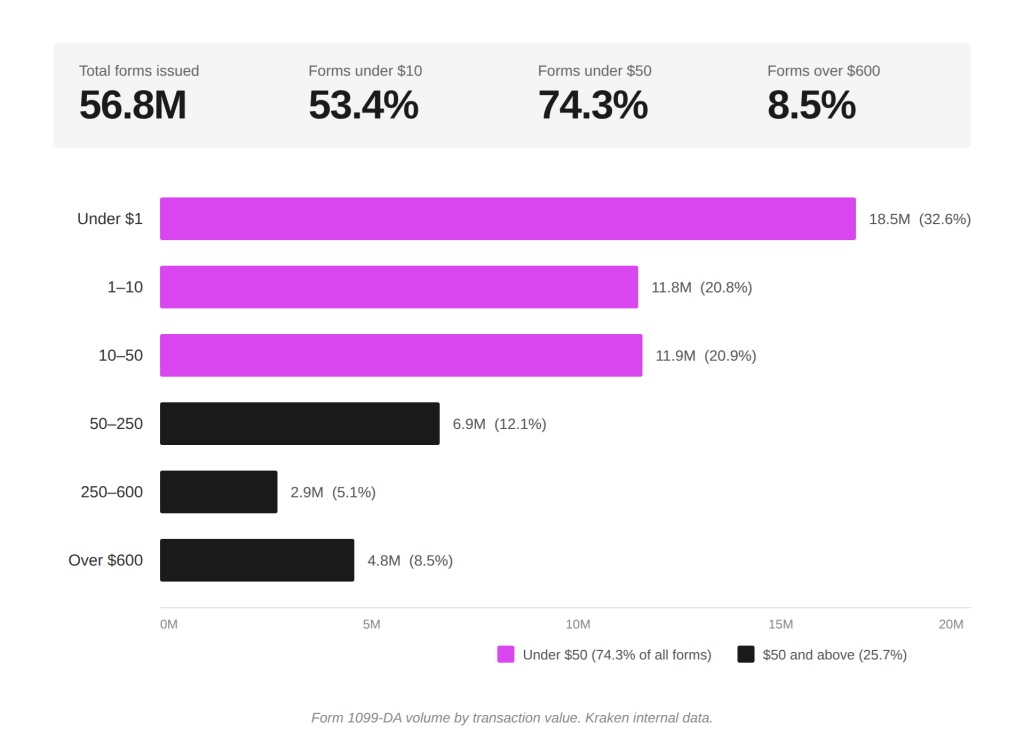

- Kraken filed 56 million crypto transaction forms with the IRS for 2025; nearly one-third covered transactions under one dollar.

- 74% of the forms covered transactions below $50, and only 8.5% exceeded the $600 threshold that triggers reporting requirements in other areas of the tax code.

- The exchange is lobbying Congress for an inflation-indexed de minimis exemption and the ability for taxpayers to choose when to pay taxes on staking rewards.

The exchange Kraken filed a total of 56 million Form 1099-DA forms with the United States Internal Revenue Service (IRS) for fiscal year 2025. Of that total, 18.5 million covered transactions below one dollar, and more than half corresponded to operations under ten dollars. Only 8.5% exceeded $600, the threshold that in most other areas of the tax code triggers the reporting obligation.

The exchange published the data alongside a clear position: the problem is not the technology, but the tax code. Each form issued implies a reconciliation task for the taxpayer, and standard tax software does not process cryptocurrency transactions. Kraken estimated that an active holder may spend between $250 and $500 annually on specialized tools alone, not counting the hours spent reconciling transactions. The Tax Foundation calculates that individual filings already cost Americans $146 billion in time and expenses.

Kraken Criticizes the Outdated Tax Code

The company identified two specific problems. The first is the absence of a de minimis exemption for everyday payments with cryptocurrencies. Under current rules, buying a hamburger with Bitcoin generates a taxable event that requires the taxpayer to calculate the cost basis of the fraction of currency used and report the gain or loss on the corresponding form. The Cato Institute noted that paying for a daily coffee with BTC can translate into more than one hundred pages of tax filings.

The second problem is the treatment of staking. Rewards are considered ordinary income at the moment of receipt, valued at the market price of that day. If the token falls in value before the filing, the taxpayer may owe taxes on an amount exceeding the current value of the asset, which Kraken calls phantom income. A significant portion of the sub-dollar forms issued corresponded precisely to staking distributions.

Legislation currently before Congress includes a de minimis provision, but limited to payment stablecoins. Kraken is asking for it to be extended to all digital assets, indexed to inflation, and accompanied by safeguards against abusive structuring. The exchange also requests that taxpayers be able to choose when to pay taxes on staking rewards: upon receipt or at the time of sale. The exchange’s systems already support both reporting methods; Congress only needs to authorize the option.