TL;DR:

- The BIS claims stablecoins function more like ETFs than real money, as their prices deviate from parity and redemptions are not guaranteed.

- The report warns that the expansion of dollar-denominated stablecoins threatens monetary sovereignty, especially in emerging economies with weak currencies.

- The BIS urges accelerating the development of tokenized money from central and commercial banks as a more robust alternative to the $316 billion stablecoin market.

The Bank for International Settlements (BIS) published its annual economic report with a critical assessment of the market for stablecoins, questioning their capacity to function as genuine money and warning about the risks their expansion poses to the global monetary system.

The BIS argues that these tokens present two structural flaws that distance them from the technical definition of money. On one hand, their prices in secondary markets frequently deviate from parity with the underlying currency, just as ETF shares diverge from their net asset value.

The BIS Annual Economic Report 2026 is out https://t.co/YV2mFvVnXi#AI #Inflation #NBFIs #PublicDebt #Stablecoins #BISAnnualEconReport pic.twitter.com/5tzGipxO4I

— Bank for International Settlements (@BIS_org) June 28, 2026

On the other, redemption mechanisms are subject to limitations, delays and costs that prevent instant and guaranteed conversion to cash. “Redemption frictions are common, suggesting that current stablecoin designs resemble exchange-traded fund shares more than means of payment,” the document states.

Involuntary Dollarization

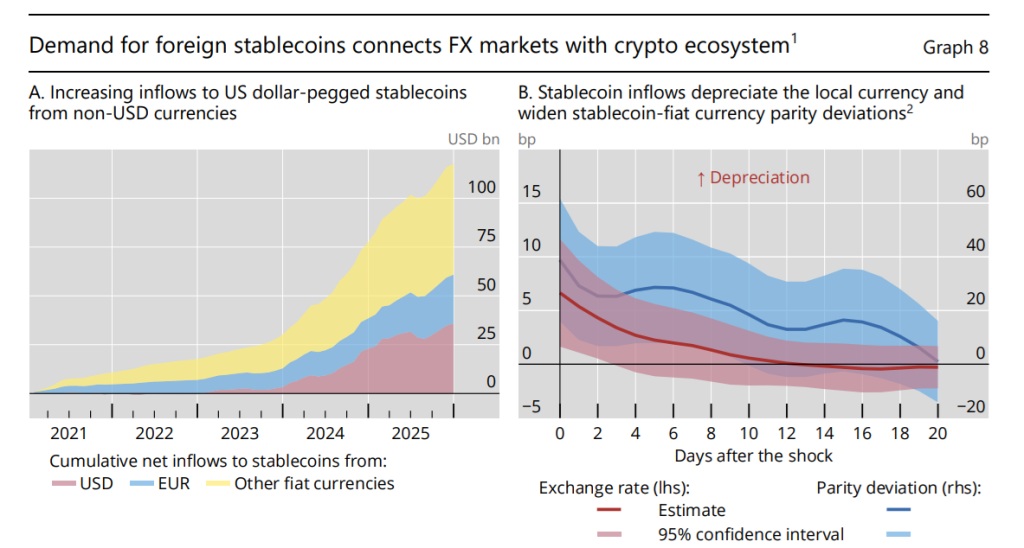

The report also identifies a phenomenon it terms “stablecoin dollarization“: the growing flow of capital from local currencies into dollar-denominated tokens. According to the BIS, this process can weaken domestic currencies in the spot market, erode the effectiveness of monetary policy and amplify exposure to volatile cross-border capital flows, particularly in emerging economies.

The institution draws a direct parallel with traditional banking dollarization, historically driven by high inflation and sovereign stress, but warns that the digital version of this phenomenon is harder to contain. The capital controls that apply to conventional bank deposits do not translate with the same effectiveness to self-custody, cross-border tokens.

BIS: Redirecting Tokenization

Faced with this diagnosis, the BIS does not propose halting tokenization as a concept, but rather redirecting it. The institution promotes a “unified ledger” architecture that combines tokenized money from central banks, tokenized deposits from commercial banks and tokenized financial assets, all within programmable platforms operating under regulated legal frameworks. That model, according to the institution, would allow the benefits of tokenization to be harnessed —programmable transactions and faster settlement— without compromising monetary stability or financial integrity.

The report also renews its criticism of public and permissionless blockchains, such as Bitcoin and Ethereum, arguing that their decentralized consensus mechanisms generate congestion, extended confirmation times and structurally high costs as activity grows, characteristics that render them unsuitable as systemic financial infrastructure.