Shiba Inu (SHIB) was a widely traded memecoin during the 2021 market cycle. Since then, its price has declined significantly from its all-time high, even as some community members point to recent headlines such as an ETF-related filing.

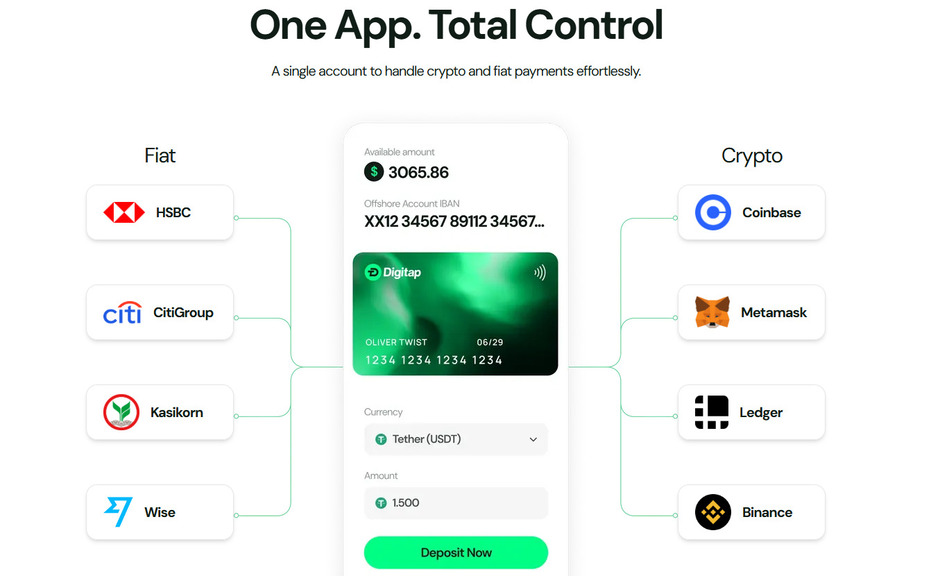

Amid this backdrop, some market participants have also been discussing an early-stage token sale for a separate project, Digitap ($TAP). The project describes itself as offering an “omni-banking” app that it says is available on Apple’s App Store and Google Play.

The project has also said it has added Visa-related functionality. This article does not verify those claims independently, and availability can vary by jurisdiction and product configuration.

Shiba Inu ETF filing and recent price action

In late October, reports circulated about an ETF-related filing connected to Shiba Inu. In one widely shared post, a crypto influencer claimed that a large asset manager had finalized an application with the US SEC. The post can be viewed here.

Market data providers show that SHIB has fallen by roughly 30% over the past month. It also remains well below its prior all-time high (a level reached several years ago), highlighting the volatility that can affect memecoins and other cryptoassets.

Separately, some commentators have continued to publish technical analysis on SHIB. For example, Coinpedia Markets posted an analysis stating that Shiba Inu has been trading within a descending channel. That post is available here.

The same analysis suggested that if SHIB breaks above a cited resistance level, it could move higher later in 2025. Such scenarios are speculative and may not play out.

Digitap’s app and Visa-related claims

Digitap has been promoted by its team as an attempt to build an “omni-bank” product that combines traditional financial services and Web3 features in one app. The project says it has released an app for iOS and Android.

According to the project, the app supports actions such as holding, transferring, swapping, and withdrawing funds across multiple fiat currencies and cryptocurrencies. Actual functionality, fees, and supported assets can vary by region and may change over time.

The project also cites user reviews suggesting that an “all-in-one” design may reduce the need to use multiple wallets, exchanges, and banking apps. These are user opinions and may not reflect every user’s experience.

Digitap states that Visa-related integration is intended to enable spending at merchants that accept Visa, subject to availability, card issuance terms, and local rules. The project also says it offers Visa cards that can be used with Apple Pay and Google Pay where supported.

Digitap also markets an onboarding flow that it describes as “No-KYC.” In practice, identity verification requirements can depend on product features, transaction limits, and regulatory obligations in different countries.

Beyond payments, the project references staking and “VIP reward tiers.” Any rewards, eligibility criteria, and risks are set by the project and can change; readers should treat such features as project-reported and not guaranteed.

Digitap token sale: project-reported figures and pricing

Digitap’s token sale has been marketed as having raised more than $1.43 million and sold more than 94 million tokens. These figures are based on project reporting and have not been independently audited in this article.

The Digitap team has said funds raised would be used for development and market expansion. The project has also stated an aim to expand its services to more than 150 countries by the end of 2026; this is a target rather than a confirmed outcome.

The project lists a current token price of $0.0268 USDT and describes a “next stage” price of $0.0297 USDT. It has also referenced an intended launch/listing price; any future listing and pricing are uncertain and depend on market conditions and exchange decisions.

The project’s materials also compare earlier token-sale pricing stages with the current stage. Such comparisons reflect token-sale pricing set by the project and are not the same as secondary-market performance.

Interest in early-stage token sales can be influenced by marketing, market sentiment, and risk appetite, and outcomes can vary widely.

How some traders are framing SHIB vs. $TAP

Some traders have compared SHIB’s drawdown from its prior highs with newer, early-stage projects such as Digitap. These comparisons are often based on differing narratives, time horizons, and risk profiles, and they do not establish that one asset is “safer” than another.

Digitap’s supporters argue that a consumer-facing app and payments features could help drive usage. Whether the product achieves broader adoption will depend on execution, compliance requirements, competition, and market conditions.

Readers should be cautious with claims about future returns or performance, particularly for early-stage tokens.

Project links (for reference):

Website: https://digitap.app

Social: https://linktr.ee/digitap.app

This article is for informational purposes only and does not constitute financial or investment advice. This outlet is not affiliated with the project mentioned.