TL;DR

- Bitcoin miners built energy infrastructure now worth more than their computing hardware.

- AI companies need exactly the power delivery systems miners spent years constructing.

- Debt markets show creditors view AI infrastructure firms as higher risk than utilities.

There is an asset Bitcoin miners spent years building without realizing it would one day be worth more than the compute itself: energy delivery infrastructure. Substations, transmission interconnections, long-term power supply agreements, operations teams capable of keeping hardware running around the clock. All of it cost billions of dollars and took years to negotiate. And now it turns out to be exactly what the artificial intelligence industry cannot build fast enough.

That is the thesis behind the migration. Not that miners abandoned Bitcoin —many still run both businesses in parallel. What they recognized was that they owned the bottleneck of the next cycle’s digital economy: installed energy capacity in grid-connected locations, already operational cooling infrastructure, and technical teams trained in high-density compute environments. Selling that capacity to AI workloads generates margins that mining, subject to Bitcoin price volatility and successive halvings, can rarely guarantee on a sustained basis.

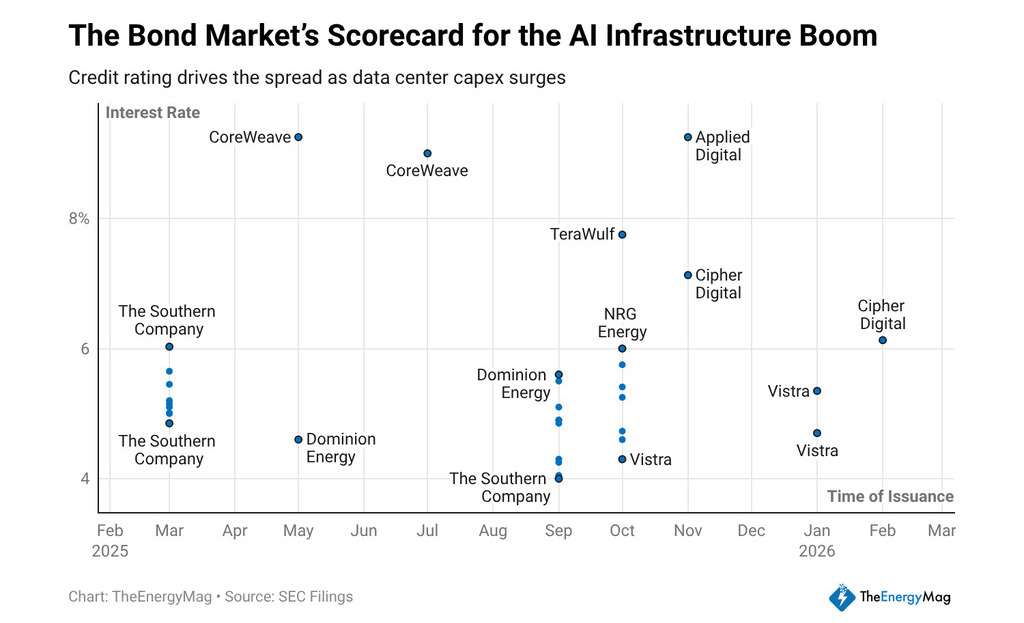

Over the past twelve months, companies in the sector raised approximately $33 billion in long-term senior notes, and the coupons they paid tell a precise story about how creditors read the model. CoreWeave closed placements at 9.25% and 9%. Applied Digital paid 9.2%. TeraWulf issued at 7.75%. Cipher Mining at 7.125% and 6.125%. All are companies traveling, to varying degrees, the same route: from mining operators to AI compute infrastructure providers.

What the Cost of Money Says About the Model

A fixed-income investor does not finance narratives —they finance cash flows. When a creditor charges an AI infrastructure company between 300 and 500 basis points more than a regulated utility, they are expressing an opinion about the predictability of those flows.

Utilities have contract-backed revenues reviewed by regulators, approved rate structures, and assets with useful lives measured in decades. Companies that migrated from mining to AI have offtake agreements —long-term supply contracts with clients committing to consume compute capacity— but creditors still do not grant them the same institutional standing.

The difference is not irrational. An offtake contract with an AI client is only as solid as that client’s solvency and the sustained demand for the models it runs. If the AI market faces a demand correction, or if customer concentration among a handful of tech companies creates counterparty risk, the cash flows from those operations become less predictable than those of a power distribution company. Creditors charge for that difference, and the coupons visible in the market reflect exactly that calculation.

For investors in digital assets, the spread carries an additional reading. The differential between what an AI infrastructure company pays and what a consolidated asset pays equals the cost of transition. Until companies in the sector accumulate enough cash flow history under long-term contracts, the credit market will keep treating them as growth bets. That pressures operating margins, because part of the cash flow they generate goes directly into servicing expensive debt.

The scale of the wager becomes clear when looking at planned electrical capacity: mining companies have approximately 30 gigawatts of new capacity in development aimed at AI workloads, nearly triple what they currently operate.

Not all of that capacity will be built on announced timelines or at projected costs —permitting delays, transmission grid constraints, and construction costs are variables that historically compress the returns announced in investor presentations. But the direction of capital is clear, and Nvidia’s results —94% earnings growth, 73% revenue growth, $68.1 billion in quarterly sales— confirm that the compute demand driving those investment decisions shows no signs of retreat.

The resulting business model combines two logics that previously operated separately

On one side, the logic of the energy infrastructure operator: maximize uptime, minimize cost per megawatt-hour, negotiate power supply contracts that protect margins against spot market volatility. On the other, the logic of the compute services provider: attract clients with intensive workloads, sign long-term contracts that justify the debt issued, and build a recurring revenue base that eventually convinces creditors to lower coupons.

The model’s success depends on whether companies manage to compress that spread before current debt matures. If in two or three years they can refinance at 5% or 6% instead of the current 9%, the business improves structurally. If offtake contracts do not renew, if clients migrate toward proprietary infrastructure, or if energy prices rise faster than compute service revenues, the fixed cost of expensive debt becomes a burden that compresses returns and forces dilution or restructuring.

For a digital asset investor evaluating exposure to the segment, the question is not whether the miners-to-AI migration makes sense as a long-term thesis —it clearly does. The question is which part of the capital structure makes sense to hold. Debt at 9% offers yield with liquidation priority, but upside is capped.

Equity captures the appreciation if the model works, but absorbs losses first if contracts do not hold. The spread on those bonds is not just a credit market data point —it is the entry price for a question that does not yet have an answer.