TL;DR

- Bitcoin sits 47% below its peak with no confirmed bottom in sight.

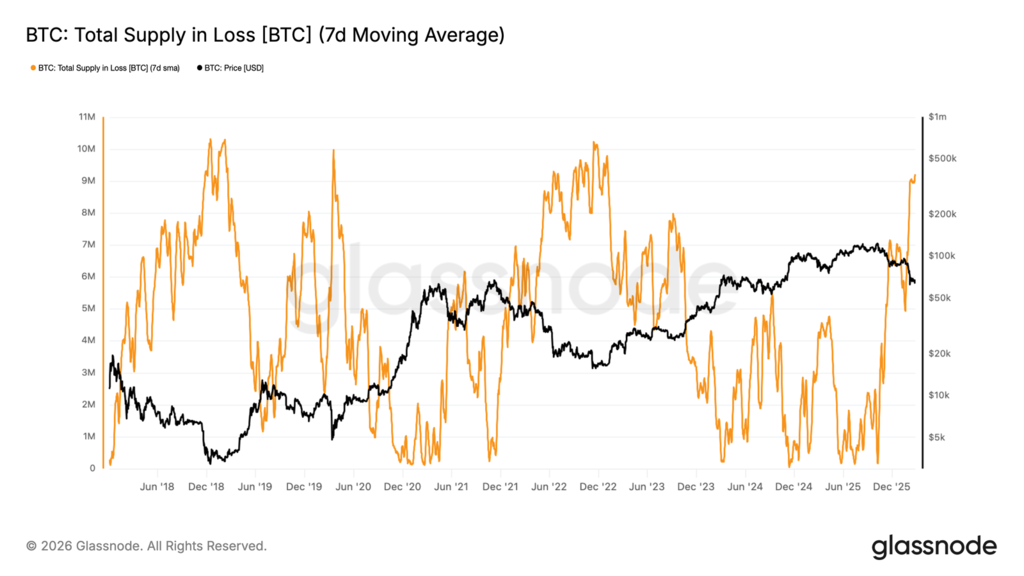

- Nearly 9.2 million BTC holders carry unrealized losses across the current range.

- Large wallet holders stopped accumulating, removing the market’s most reliable upside support.

There are moments in financial markets where stillness communicates more than movement. Bitcoin has spent several weeks inside one of those moments. The price drifts between $60,000 and $70,000, refusing to break lower with determination or recover with conviction. What reads as stability on the surface conceals something less comfortable underneath: a market that isn’t healing, just not bleeding out.

The distinction between those two conditions carries more weight than most participants acknowledge. A market that simply avoids collapse can remain suspended for months, grinding down both financial capital and the psychology of anyone positioned inside it. Taken together, the metrics available right now describe exactly that environment — an asset caught in a fragile equilibrium where sellers ran out of energy before buyers showed up to replace them.

Bitcoin sits 47% below its all-time high

At that drawdown depth, the historical record places the asset in territory associated with the middle-to-late stages of prior bear cycles. In May 2022, the market spent weeks consolidating at a comparable distance from its peak before resuming its decline. History doesn’t guarantee repetition, but it generates a probability map that investors with cycle memory read carefully. The current coordinates on that map do not point toward early recovery.

Roughly 9.2 million bitcoins now sit with owners who paid more than the current price. Nearly half the circulating supply carries unrealized losses. A number that large doesn’t describe isolated pockets of distress — it describes a condition distributed across a wide range of holder cohorts, one that historically has appeared in the later rather than the earlier stages of bear markets.

The constructive reading is that broad pain of that magnitude has preceded market bottoms before. The cautious reading is that none of the signals typically associated with a confirmed bottom have materialized yet.

The Entities With the Most Capital Are Watching, Not Buying

The metric tracking accumulation intensity across wallet cohorts — weighted to assign greater influence to larger holders — has stayed below 0.5 for weeks. On a scale from zero to one, that level doesn’t describe active accumulation. It describes calculated indifference.

Large holders aren’t selling aggressively, which removes one of the more pessimistic scenarios from the table. But they aren’t buying with the conviction that has historically preceded durable recoveries either.

The ratio comparing gains to losses materialized over the past ninety days dropped below 1.0 — the threshold separating a market where profit-taking dominates from one where loss realization takes over. Every prior instance of a sustained break below that level extended for six months or longer before reversing. That isn’t a prediction; it’s a description of how long liquidity typically takes to rebuild after sellers dominate the tape.

Spot market flows confirm seller dominance directly

The cumulative volume delta — the metric measuring whether the market executes more buy orders or sell orders at the margin — hit its most negative readings in two years. The recent price decline didn’t happen because buyers passively stepped away. It happened because active sellers placed market orders and forced price lower with intent.

The difference between those two mechanisms matters for what comes next: passive buyer absence resolves more quickly than active distribution.

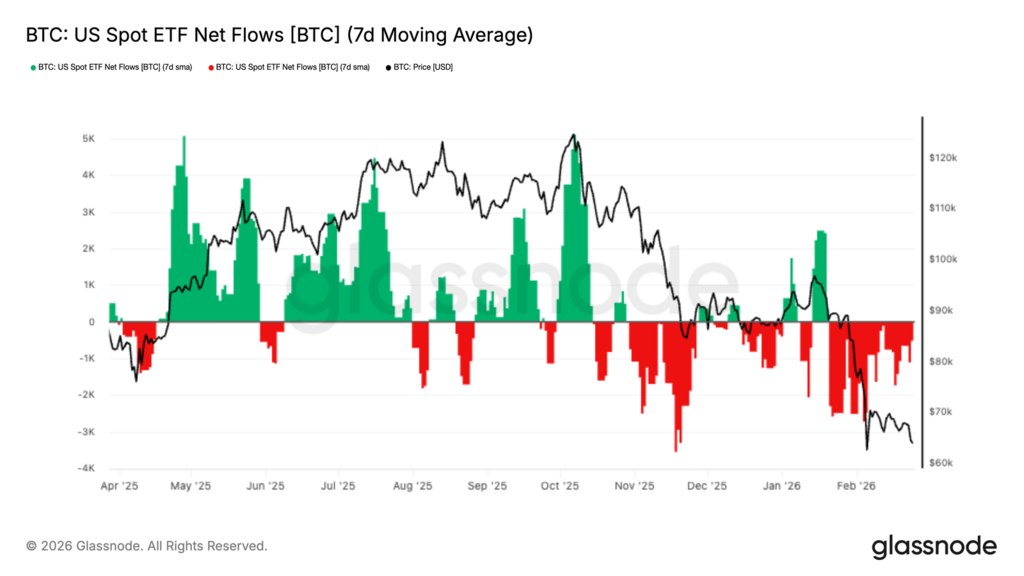

US spot Bitcoin ETFs extended their streak of net outflows from late November onward. Earlier in the cycle, strong inflow periods aligned visibly with price expansions. Today, the pattern reversed: redemption pressure persists and no flow data suggests an imminent turn.

The institutional demand that provided structural support during prior rallies offers no equivalent bid in the current environment. Removing that support doesn’t cause collapse on its own, but it eliminates a cushion that many market participants had grown accustomed to treating as permanent.

Perpetual futures funding rates returned to neutral after the correction, which means the cycle cleared its excess of leveraged long exposure. The positive interpretation: no large pool of forced long liquidations sits waiting to push price mechanically lower.

The less encouraging interpretation: the absence of positive funding also reflects absent speculative appetite — exactly the kind of energy that has historically powered the early stages of sustained recoveries. A clean derivatives market is a prerequisite for recovery, not evidence that recovery started.

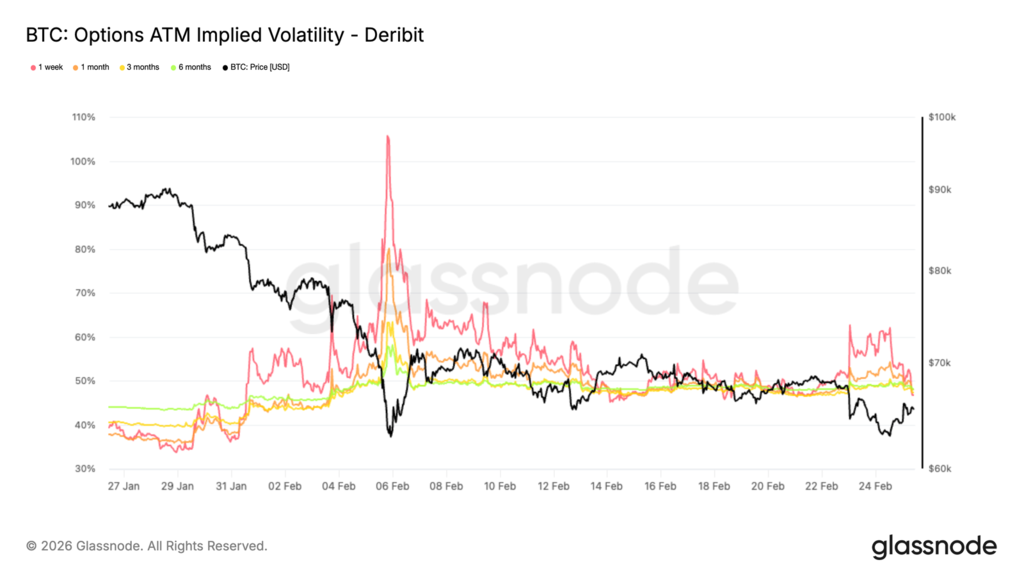

When Bitcoin approached $62,000 in recent sessions, one-week implied volatility jumped from 47% to 62% as participants rushed to buy short-term protection. When price recovered to $65,000, volatility compressed back to 47% within days.

That rapid expansion and equally rapid collapse describes a reactive market, not one pricing systemic stress. Traders pay for protection near key support levels and abandon it the moment the immediate threat recedes. Fear arrives in spikes, not sustained waves.

The gap between put and call pricing tells a more defensive story

Downside puts trade at nearly a 30% premium over upside calls, matching the asymmetry last recorded during the sharp drop toward $60,000 in early February.

Each bounce from the lower end of the range generates fresh demand for downside hedges, signaling that participants use recoveries to rebuild insurance rather than increase directional exposure. When a market treats rallies primarily as opportunities to protect against further losses, it reveals something about where conviction actually sits.

Between $55,000 and $70,000, dealers carry net negative gamma exposure, obligating them to sell as price falls and buy as price rises. That mechanism doesn’t set the direction of any move, but it accelerates whatever move is already underway. In a low-liquidity environment, acceleration of that kind can turn moderate displacements into sharp ones without any new fundamental catalyst.

Bitcoin isn’t broken. But the conditions required for a durable recovery aren’t in place yet. The market processes accumulated losses, clears leveraged positions, and waits for an actor with sufficient capital to decide the current price justifies a conviction-sized bet. Until flows confirm that actor arrived, the $60,000 to $70,000 range functions less like a floor and more like a waiting room where the next directional decision gets made.